|

Photo: Odd Kristian Dahle/Fishing boat.

SINTEF report: The sea fishing fleet creates values worth US$ 3,32 billion

NORWAY

NORWAY

Monday, November 28, 2022, 05:00 (GMT + 9)

The total value creation contribution of sea-going fishing fleets in Norway in 2021 was NOK 32.8 billion including ripple effects. This value creation employed approximately 21,000 man-years, shows a new SINTEF report.

The importance of the ocean-going fleet is between 61-66 per cent of the entire fishery-based value chain. This is shown in a recently prepared report from SINTEF Ocean on behalf of Fiskebåt. The importance of the ocean-going fleet is between 61-66 per cent of the entire fishery-based value chain. This is shown in a recently prepared report from SINTEF Ocean on behalf of Fiskebåt.

The fishery-based value chain includes the catch link, fish processing (based on wild fish/shellfish/shellfish) and the export/trade link, as well as suppliers of services and equipment for the various parts of the value chain. The sea fishing sector itself consisted of 4,500 man-years in 2021. The sector's contribution to GDP was NOK 11.4 billion in 2021.

The catch link is the origin of extensive ripple effects

Demand from the fishing sector leads to activity at companies that supply goods and services to the industry, these amounted to 4.4 billion. In addition, the activity going forward in the value chain, i.e. as a result of the fleet's deliveries, is of great importance, especially when it comes to employment and value creation in the fish processing industry. This contribution was NOK 18 billion. The ocean-going fishing fleet contributed to total value creation both upstream and downstream in the entire Norwegian fisheries value chain of NOK 21.4 billion and 16,500 man-years in 2021. The total for the entire value chain is NOK 32.8 billion and 21,000 man-years.

Each man-year in the ocean-going fishing fleet gives rise to a further 3.5 man-years in the value chain. In total, the fishing section of the ocean-going fishing fleet creates a value creation contribution of approx. 2 kroner in addition to every kroner created by the industry itself.

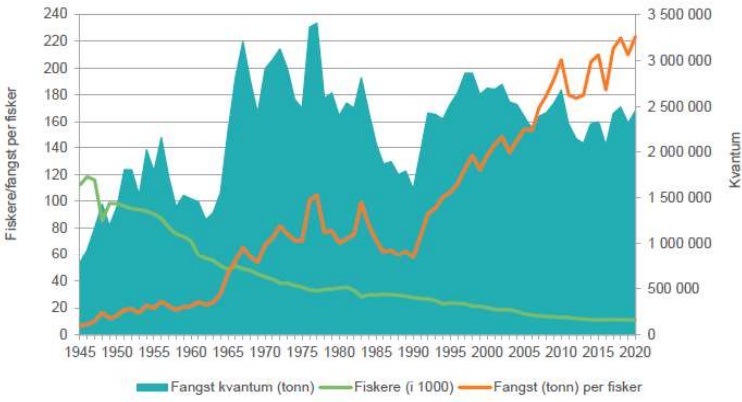

Catch, fishermen and catch per fisherman 1945-2020.

Continuous growth from the 90s

Productivity growth in the fishing fleet has risen significantly and almost continuously from the beginning of the 90s until today's level. E.g. catch per employed fisherman has more than tripled in this period. Larger and more efficient fishing vessels and gear are a significant reason.

The operating margin in the fleet has increased from 5-6% annually in the early 80s to an average of around 20% in recent years. The largest vessels have the best operating margin (20-25%), while the losing vessels have the lowest, i.e. between 5-10%. In comparison, all limited companies in Norway (except financial companies) achieved an average operating margin of 9.3% for the years 2019-2021.

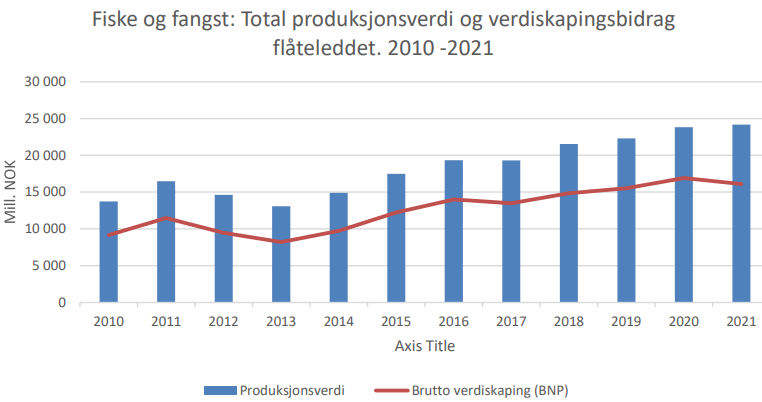

Production value and value creation contribution from the fishing fleet 2010 2021. The figures show values isolated to the fleet segment, excluding ripple effects.Source: SINTEF Ocean.

With several important stocks close to maximum long-term biological yield, and the fact that the costs of the input factors are in an inflationary period, one will at best have to expect a flattening of further growth at a high level. Much will depend on global efforts to control further inflation and that the global markets have the purchasing power to demand top seafood from Norway to the same extent as they have done in the last 10 years.

Two leading vessel groupings within the ocean-going fishing fleet

Cod trawls and purse seiners form a dominant position within the HAV fleet. The cod trawl fleet accounts for 35% of total values in terms of turnover, value creation and employment. Ringed snipe are not far behind, with 32% and 33% of the total in terms of turnover and contribution to value creation. Employment in the purse seine fleet, on the other hand, only accounts for 23% of total employment. On the other hand, the group Conventional sea fishing vessels and Offshore crab vessels have a markedly greater employment factor than they have for catch value and value creation contribution.

Source: SINTEF Ocean.

About the survey

Over several years, SINTEF Ocean has carried out analyzes of the national importance of the seafood industry. The national value creation analyzes have included both the fishery-based and the aquaculture-based value chain, as well as the seafood industry as a whole. On behalf of Fiskebåt, SINTEF Ocean has carried out a separate analysis in the autumn of 2022 where we only look at the sea-based part of the fisheries-based value chain in Norway and associated ripple effects.

Source: Fiskebat / Sintef (translated from original in norwegian)

[email protected]

www.seafood.media

|

Print

Print