|

International squid prices could begin a phase of moderate increases later in the season. Photo: China Ocean Squid Index/FIS

Global Squid Market Tightens as Latin American Catches Slow and Chinese Prices Edge Up

WORLDWIDE WORLDWIDE

Tuesday, March 17, 2026, 00:10 (GMT + 9)

Declining harvests in Peru and Argentina begin to reshape supply dynamics while fuel costs and post-holiday demand support prices

The global squid market is entering a new phase of adjustment in mid-March, as declining catches in Latin America begin to influence pricing trends in China, the world’s largest seafood import market. While supplies remain relatively abundant, early signs of tightening harvest volumes are beginning to support wholesale prices as reported by Food World.

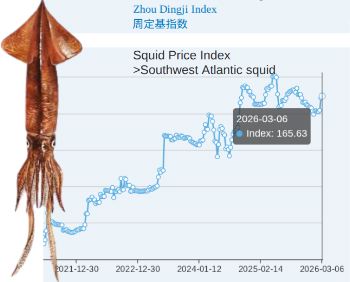

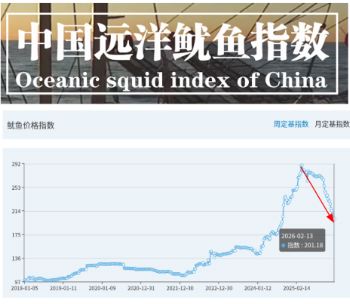

According to market data for the week ending March 12 (Week 11), the wholesale price of 1–2 kg Peruvian giant squid fillets in China increased by approximately RMB 250 per ton (about US$35 per ton). Prices for 200–300 g Argentine squid rose by roughly RMB 500 per ton (about US$70 per ton) compared with the previous week, although overall price levels have remained relatively stable. According to market data for the week ending March 12 (Week 11), the wholesale price of 1–2 kg Peruvian giant squid fillets in China increased by approximately RMB 250 per ton (about US$35 per ton). Prices for 200–300 g Argentine squid rose by roughly RMB 500 per ton (about US$70 per ton) compared with the previous week, although overall price levels have remained relatively stable.

Industry observers say the Chinese seafood market is still recovering from the consumption slowdown that typically follows the Spring Festival. A market report released on March 9 by the Zhoushan International Agricultural Products Trade Center in Zhejiang Province indicates that wholesalers are currently focused on measured restocking, with downstream demand gradually returning to normal levels.

Although consumer demand has yet to surge, steady replenishment activity in wholesale markets is providing baseline support for squid prices.

Rising Fuel Costs Add Pressure

Beyond demand dynamics, operating costs are also influencing market conditions. Recent geopolitical tensions in the Middle East have pushed global fuel prices higher, increasing operating expenses for deep-sea fishing fleets.

Because fuel represents a major portion of operational costs for distant-water fishing vessels, the rise in fuel prices is effectively raising the price floor for squid products, preventing further declines in wholesale prices.

Photo: Stockfile / FIS

Peru’s Giant Squid Catch Slows

Meanwhile, fishing activity in key production areas is beginning to slow.

Data from the Peruvian Ministry of Production shows that by March 10, Peru’s cumulative catch of giant squid (Dosidicus gigas) reached 140,915.9 tons, representing 78.64% of the 179,188-ton quota allocated for the January–April 2026 fishing season.

At the beginning of March, daily catches exceeded 2,000 tons, but volumes dropped significantly after March 7, falling to about 532 tons per day by March 10—a clear sign that harvesting activity is losing momentum.

Artisanal fishing of giant squid (dosidicus gigas) in Peru. Photo: YouTube

Fishing fleets operating outside Peru’s exclusive economic zone have also reduced activity levels.

For Chinese distant-water vessels, the average daily catch recently stood at roughly 2–3 tons per vessel. Since December 2025, the average cumulative catch per vessel has reached around 350 tons, indicating that overall production remains comparatively high despite the recent slowdown.

Argentine Squid Efficiency Declines

A similar pattern is emerging in the Argentine squid fishery (Illex argentinus). Reports from Argentine fisheries media indicate that the average daily catch per vessel has fallen sharply—from a peak of 36.3 tons to roughly 14 tons, reflecting a notable drop in fishing efficiency.

Illex squid jigging fishery in Argentina. Photo: Stockfile / FIS

Despite this decline, annual production remains historically strong. As of March 3, Argentina’s cumulative squid landings reached 123,679 tons, marking a 99% increase year-on-year and maintaining one of the highest production levels on record.

Outlook: Prices May Firm as Peak Season Passes

Overall, analysts believe the global squid market will remain well supplied in the short term. However, as the peak fishing season gradually winds down, a combination of declining catch volumes, higher fuel costs, and steady restocking demand in China is strengthening price support.

Industry insiders widely expect that if fishing volumes continue to tighten in the coming weeks, international squid prices could begin a phase of moderate increases later in the season.

Related News:

🇯🇵 日本語版 (Japanese Translation)

ラテンアメリカの漁獲減少で世界のイカ市場が引き締まり、中国で価格が上昇

ペルーとアルゼンチンで漁獲量が減少し、燃料コストと祝日後の需要が価格を支える

世界のイカ市場は3月中旬に入り、新たな調整局面に入りつつある。ラテンアメリカの主要生産地域で漁獲量が減少し始めたことで、世界最大の水産物輸入市場である中国で価格動向に影響が出始めている。具体的には、ペルー産アメリカオオアカイカの価格はやや上昇し、アルゼンチンイカの価格は全体として安定しているものの、今後さらに上昇する可能性があると市場では見られている。これはFood Worldの報道による。

3月12日までの週(第11週)の市場データによると、中国市場における1〜2kgのペルー産アメリカオオアカイカのフィレの卸売価格は、**1トン当たり約RMB 250(約US$35)上昇した。また、200〜300gのアルゼンチンイカの価格は前週比で約RMB 500(約US$70)**上昇したが、全体的な価格水準は比較的安定している。

業界関係者によると、中国の水産市場は依然として春節後の消費回復段階にある。浙江省の舟山国際農産物貿易センターが3月9日に発表した市場レポートによれば、卸売業者は現在合理的な在庫補充に重点を置いており、下流需要は徐々に通常レベルへ戻りつつある。

消費者需要の急激な増加はまだ見られないものの、卸売市場での安定した補充需要がイカ価格の基礎的な支えとなっている。

燃料コストの上昇が市場に圧力

需要面に加え、操業コストの変化も市場に影響を与えている。最近の中東の地政学的緊張により世界的な燃料価格が上昇し、遠洋漁業船団の運営コストが増加している。

燃料は遠洋漁業船の運営コストの大部分を占めるため、燃料価格の上昇は実質的にイカ製品の価格下限を押し上げ、卸売価格のさらなる下落を抑制している。

ペルーのアメリカオオアカイカ漁獲が減速

一方、主要生産地域では漁獲活動の減速が見られ始めている。

ペルー生産省のデータによると、3月10日時点でペルーのアメリカオオアカイカ(Dosidicus gigas)の累計漁獲量は140,915.9トンに達し、2026年1月〜4月漁期に割り当てられた179,188トンの漁獲枠の**78.64%**を占めている。

3月初旬には1日当たりの漁獲量が2,000トン以上に達していたが、3月7日以降は急減し、3月10日には約532トン/日まで低下した。これは漁獲活動の勢いが鈍化していることを示している。

また、ペルーの排他的経済水域外で操業する漁船団も活動を減らしている。

中国の遠洋漁業船の場合、最近の1隻あたり平均日漁獲量は約2〜3トンとなっている。2025年12月以降、1隻あたり累計平均漁獲量は約350トンに達しており、最近の減速にもかかわらず全体の生産量は比較的高い水準を維持している。

アルゼンチンイカの漁獲効率が低下

同様の傾向はアルゼンチンイカ漁業(Illex argentinus)でも見られる。アルゼンチンの水産メディアによる報道では、1隻あたり平均日漁獲量が36.3トンのピークから約14トンまで急落しており、漁獲効率の大幅な低下を示している。

それでも年間生産量は依然として歴史的に高い水準にある。3月3日時点で、アルゼンチンの累計水揚げ量は123,679トンに達し、前年比99%増を記録し、過去最高水準の一つを維持している。

見通し:ピークシーズン終了に伴い価格は上昇の可能性

全体として、アナリストは世界のイカ供給は短期的には依然として豊富であると見ている。しかし、漁獲シーズンのピークが徐々に過ぎるにつれ、漁獲量の減少、燃料コストの上昇、そして中国での安定した補充需要が組み合わさり、価格の下支えが強まっている。

業界関係者の多くは、今後数週間で漁獲量の引き締まりが続けば、国際的なイカ価格は今シーズン後半にかけて緩やかな上昇局面に入る可能性があると予想している。

🇨🇳 简体中文版 (Simplified Chinese Translation)

拉丁美洲渔获减少推动全球鱿鱼市场收紧,中国价格小幅上涨

秘鲁和阿根廷捕捞量下降,同时燃料成本与节后需求支撑价格

进入3月中旬,全球鱿鱼市场开始出现新的调整迹象。随着拉丁美洲主要生产区域的捕捞量开始下降,这一变化正逐步影响全球最大水产品进口市场中国的价格走势。具体而言,秘鲁巨型鱿鱼价格小幅上涨,而阿根廷鱿鱼价格整体保持稳定,但市场普遍认为仍存在进一步上涨的空间。以上信息来自Food World的报道。

截至3月12日当周(第11周)的市场数据显示,中国市场1–2公斤秘鲁巨型鱿鱼鱼片的批发价格上涨约RMB 250/吨(约US$35/吨)。与此同时,200–300克阿根廷鱿鱼价格较前一周上涨约RMB 500/吨(约US$70/吨),整体价格水平仍保持相对稳定。

行业观察人士表示,中国水产品市场仍处于春节后的消费恢复阶段。浙江省舟山国际农产品贸易中心在3月9日发布的一份市场报告指出,目前批发市场采购主要以理性补库为主,下游需求正在逐步恢复至正常水平。

虽然终端消费需求尚未出现明显激增,但批发市场稳定的补货需求正在为鱿鱼价格提供基础支撑。

燃料成本上升带来市场压力

除了需求因素外,运营成本的变化也在影响市场。近期中东地区地缘政治紧张局势导致全球燃料价格明显上涨,从而推高远洋渔船队的运营成本。

由于燃料是远洋捕捞作业的重要成本组成部分,燃料价格上涨实际上正在抬高鱿鱼产品的价格底线,限制了批发价格进一步下跌的空间。

秘鲁巨型鱿鱼捕捞速度放缓

与此同时,主要生产区域的捕捞活动开始出现放缓迹象。

秘鲁生产部数据显示,截至3月10日,秘鲁巨型鱿鱼(Dosidicus gigas)累计捕捞量达到140,915.9吨,占2026年1月至4月捕捞配额179,188吨的78.64%。

在3月初,每日捕捞量一度超过2,000吨,但自3月7日起显著下降,到3月10日已降至约532吨/日,表明资源捕捞速度正在放缓。

在秘鲁专属经济区之外作业的远洋船队活动也有所减少。

对于中国远洋渔船而言,近期单船平均日捕捞量约为2–3吨。自2025年12月以来,单船累计平均捕捞量已达到约350吨,表明尽管近期有所放缓,但整体产量仍处于较高水平。

阿根廷鱿鱼捕捞效率下降

类似的变化也出现在阿根廷鱿鱼渔业(Illex argentinus)。阿根廷渔业媒体报道称,单船平均日捕捞量已从36.3吨的峰值下降至约14吨,显示捕捞效率明显下降。

不过,从年度数据来看,阿根廷鱿鱼资源仍处于高产周期。截至3月3日,当地累计卸货量达到123,679吨,同比增长99%,并保持在历史高位之一。

展望:随着旺季结束,价格可能逐步走强

整体来看,分析人士认为全球鱿鱼供应在短期内仍将保持相对充足。然而,随着捕捞旺季逐渐过去,产量下降、燃料成本上升以及中国稳定的补库需求共同作用,正在增强市场对价格的支撑。

业内人士普遍预计,如果未来几周捕捞量继续收紧,国际鱿鱼价格可能在本季后期进入温和上涨阶段。

[email protected]

www.seafood.media

|

Print

Print