|

The industry in Europe reduced the use of wild-caught fish per kilogram produced by 59% through substitution with soy protein concentrate and rapeseed

Indefinite Moratorium in Peru and Structural Supply Gap in Asia Trigger Global Fishmeal and Fish Oil Price Surge

WORLDWIDE WORLDWIDE

Monday, June 22, 2026, 00:10 (GMT + 9)

Suspension of industrial anchovy catches aggravates shortages across aquaculture markets, forcing historic low inclusion rates in commercial diets and driving up premiums for Omega-3 specifications

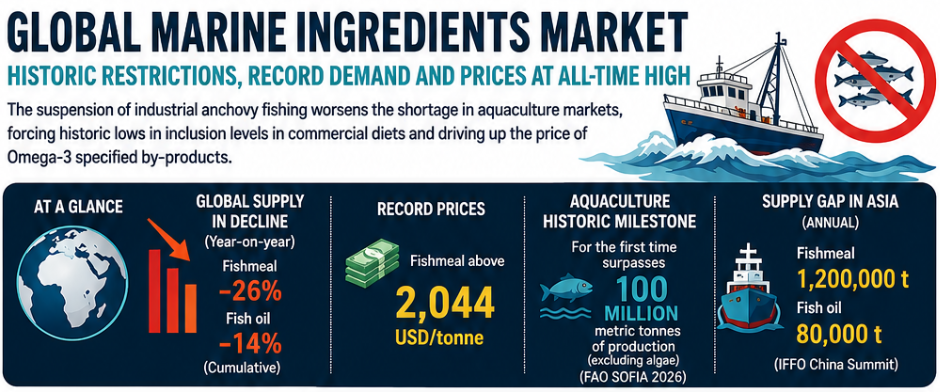

The global marine ingredients market is facing a scenario of severe supply constraints throughout this month of June 2026. The convergence of strict biological management measures in South America and historically expanding aquaculture demand has locked in a structural imbalance, keeping international prices at record highs.

Click on the image to enlarge

Peru Prolongs Fishing Ban Due to Ocean Anomalies

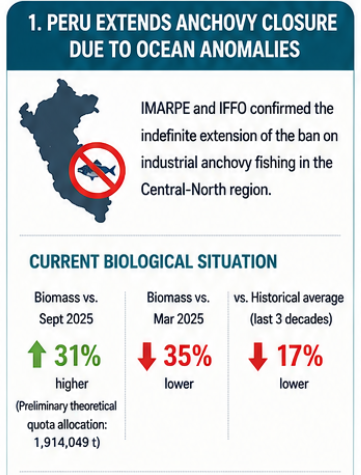

The Institute of the Marine of Peru (IMARPE) and The Marine Ingredients Organisation (IFFO) confirmed the indefinite extension of the industrial fishing ban for anchovy (Engraulis ringens) in the strategic North-Central region, a measure originally scheduled to expire on June 10, 2026.

Technical monitoring confirms the persistence of thermal anomalies linked to a Coastal El Niño scenario. Although exploratory fishing operations detected a biological volume 31% higher than that recorded in September 2025 —suggesting a preliminary theoretical quota allocation of 1,914,049 metric tons— the current biomass sits 35% below March 2025 levels and 17% lower than the historical average of the last three decades. Due to a high incidence of juvenile specimens, the main Steam Dried (SD) processing plants in Chimbote and Callao remain under preventive technical shutdowns to safeguard recruitment.

As a direct consequence, cumulative global fishmeal production reports a year-on-year contraction of 26%, while global fish oil supply falls back by 14%. This widespread shortage is holding the international benchmark price above 2,044 USD per ton. In parallel, to secure access to the European market amid the stringent requirements of the EU Deforestation Regulation (EUDR), Peruvian fishing company Austral Group became the first in the country this month to validate the Life Cycle Assessment (LCA) of its marine ingredients using the international methodology of the Global Feed LCA Institute (GFLI).

Historic Aquaculture Milestone and Supply Gap in Asia

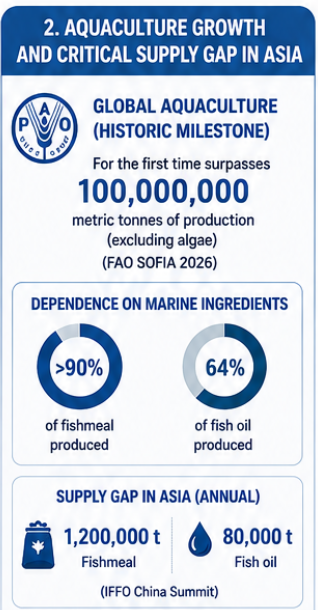

This supply squeeze coincides with a sectoral milestone formally reported by the FAO in its SOFIA 2026 report issued on June 17, 2026: global aquaculture production has surpassed 100,000,000 metric tons for the first time (excluding algae). This exponential growth has intensified reliance on marine inputs, with aquaculture now absorbing more than 90% of global fishmeal and 64% of global fish oil production. This supply squeeze coincides with a sectoral milestone formally reported by the FAO in its SOFIA 2026 report issued on June 17, 2026: global aquaculture production has surpassed 100,000,000 metric tons for the first time (excluding algae). This exponential growth has intensified reliance on marine inputs, with aquaculture now absorbing more than 90% of global fishmeal and 64% of global fish oil production.

The impact of this pressure was rigorously analyzed at the IFFO China Summit, which revealed a critical regional supply gap (Supply Gap) in Asia reaching 1,200,000 metric tons annually for fishmeal and 80,000 metric tons for fish oil destined for aquafeed formulation.

In the mainland Chinese domestic market, demand has fragmented into highly specialized niches (species such as eel, shrimp, and California bass), which demand very specific digestible amino acid profiles. Feed manufacturing companies are facing severe difficulties in balancing formulation costs. At the ports of Qingdao and Shanghai, the spot price for imported Peruvian fishmeal (Super Quality) remains firm in a range of 22,900 to 23,000 RMB per metric ton (approximately 3,158 to 3,172 USD).

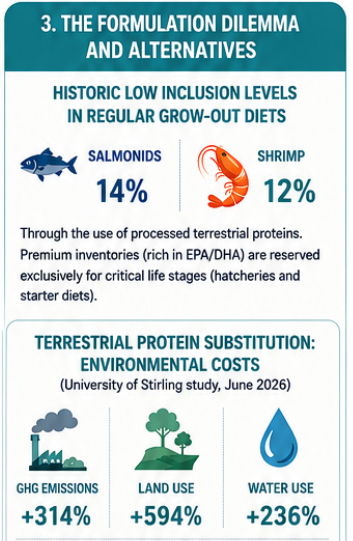

The Technical Formulation Dilemma and Alternatives

Faced with the price crisis, technical platforms such as Aquafeed.com confirm that nutrition giants like Cargill and Skretting are executing a strategic pivot, reducing standard inclusion rates in regular grower diets to historic lows of 14% in salmonids and 12% in shrimp through the use of processed terrestrial proteins. Premium fishmeal and high-EPA/DHA oil inventories are being strictly reserved for strategic use in critical lifecycle stages (hatcheries and starter diets).

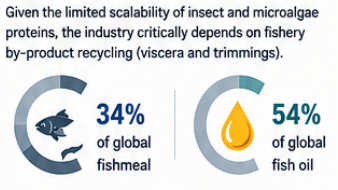

However, total substitution presents severe environmental complications. A long-term study by the University of Stirling published by the Responsible Seafood Advocate in June 2026 demonstrated that while the industry in Europe reduced the use of wild-caught fish per kilogram produced by 59% through substitution with soy protein concentrate and rapeseed oil, this triggered a sharp increase in the integrated terrestrial environmental footprint: greenhouse gas (GHG) emissions rose by 314%, land use by 594%, and water consumption by 236%. Given that insect proteins and microalgae have yet to scale commercially to mitigate these costs, the industry relies critically on the recycling of fishery by-products (trimmings and offal), which today already account for 34% of global fishmeal and 54% of global fish oil.

Macroeconomic Adjustments and By-Product Distortions

The latest global balance from GLOBEFISH (FAO) confirms that the shortage stemming from the Peruvian standstill is exacerbated by restrictions in other producing countries. Chile applied a 44% technical cut to its anchovy quotas, setting them at 625,000 metric tons, neutralizing the stability brought by the 1,200,000 metric tons of horse mackerel.

Buying pressure from salmon industries in Norway and Chile is absorbing critical volumes, limiting exportable surpluses. At the same time, trade flows show a sharp reconfiguration in South America: Ecuador has consolidated its buying position for shrimp aquaculture, drastically lifting its imports of Peruvian fishmeal from 17,000 to 46,000 metric tons.

Finally, FAO technical analysis highlights an unprecedented inflection in the fats market: fish oil with nutraceutical and pharmaceutical specifications has consolidated a price premium of 2,044 USD per metric ton above commercial grade (feed-grade), reflecting the rigid and total inelasticity of demand in high-purity sectors.

🇯🇵 Japanese Version

ペルーの無期限禁漁とアジアの構造的供給ギャップが世界の魚粉・魚油価格の急騰を引き起こす

産業用カタクチイワシ漁の停止が水産養殖市場の供給不足を悪化させ、商業用飼料における配合率を歴史的低水準に追い込み、オメガ3仕様の副産物プレミアムを押し上げる

ロンドン(Fish Info & Services) – 世界の海洋原料市場は、この2026年6月の間、極めて深刻な供給制限シナリオに直面している。南米における厳格な生物学的管理措置と、歴史的な拡大を続ける水産養殖需要の合流が構造的な需給不均衡を定着させ、国際価格を記録的な高値に維持している。

海洋異変によりペルーが禁漁を延長

ペルー海軍海洋研究所(IMARPE)と国際海洋原料組織(IFFO)は、戦略的な中北部地域におけるカタクチイワシ(Engraulis ringens)の産業用禁漁措置の無期限延長を確認した。この措置は当初、2026年6月10日に失効する予定であった。

技術的なモニタリングにより、沿岸のエルニーニョ現象に関連する熱異常の継続が確認されている。調査漁業では2025年9月の計測値を31%上回る生物量が検出され、1,914,049トンの暫定的な理論枠の割り当てが示唆されたものの、現在の現存量は2025年3月の水準を35%下回り、過去30年間の歴史的平均よりも17%低い。未成魚(幼魚)の混獲率が非常に高いため、チンボテおよびカヤオにある主要な直火乾燥(SD)魚粉加工工場は、資源の加入を保護するために予防的な技術操業停止を続けている。

直接的な結果として、世界累計の魚粉生産量は前年同期比26%減少を記録し、世界の魚油供給量は14%後退している。この世界的な供給不足により、国際指標価格はトン当たり2,044米ドルを上回る水準で推移している。並行して、欧州の森林破壊規制(EUDR)の厳格な要件の中で欧州市場へのアクセスを確保するため、ペルーの漁業会社Austral Groupは今月、国際組織であるGlobal Feed LCA Institute(GFLI)の国際手法に基づき、同国の海洋原料のライフサイクルアセスメント(LCA)を検証した最初の企業となった。

水産養殖の歴史的節目とアジアの供給ギャップ

この供給の絞り込みは、2026年6月17日に発表されたFAOのSOFIA 2026報告書で公式に示されたセクターの歴史的節目と重なっている。世界の水産養殖生産量は、初めて100,000,000トン(藻類を除く)を突破した。この指数関数的な成長は海洋原料への依存を強めており、現在、水産養殖は世界の魚粉生産量の90%以上、魚油生産量の64%を吸収している。

この圧力の影響はIFFO China Summitで厳密に分析され、アジア地域における深刻な供給ギャップ(Supply Gap)が、水産養殖飼料配信用として魚粉で年間1,200,000トン、魚油で80,000トンに達していることが明らかになった。

中国本土の国内市場では、需要が高度に専門化されたニッチ(ウナギ、エビ、オオクチバスなどの魚種)に断片化しており、これらは非常に特定の可消化アミノ酸プロファイルを要求している。飼料製造企業は、配合コストのバランスを取る上で深刻な困難に直面している。青島および上海の港では、ペルーから輸入された魚粉(スーパー品質)の現物価格がトン当たり**22,900〜23,000人民元(約3,158〜3,172米ドル)**の範囲で堅調に推移している。

配合の技術的ジレンマと代替原料

価格危機に直面し、Aquafeed.comなどの技術プラットフォームは、CargillやSkrettingといった栄養大手が戦略的な転換を実行していることを確認している。陸生加工タンパク質を使用することで、通常の成育用飼料における標準配合率をサケ・マス類で14%、エビで12%という歴史的低水準に引き下げている。プレミアム魚粉および高EPA/DHA魚油の在庫は、重要なライフステージ(孵化場や初期飼料)における戦略的利用のために厳格に確保されている。

しかし、完全な代替は深刻な環境問題を提示している。スターリング大学が2026年6月にResponsible Seafood Advocateで発表した長期研究では、欧州の産業が大豆タンパク質濃縮物や菜種油への代替により、生産キログラム当たりの天然魚の使用量を59%削減したものの、これが陸域の総合的な環境フットプリントの急増を引き起こしたことが実証された。温室効果ガス(GHG)排出量は314%、土地利用は594%、水消費量は236%増加した。昆虫タンパク質や微細藻類は、これらのコストを緩和するための商業的スケールにまだ達していないため、業界は漁業副産物(残渣や内臓)のリサイクルに決定的に依存しており、これは現在すでに世界の魚粉の34%、世界の魚油の54%を占めている。

マクロ経済調整と副産物の歪み

FAOのGLOBEFISHによる最新の世界バランスは、ペルーの停滞に起因する不足が他の生産国の制限によって悪化していることを確認している。チリはカタクチイワシの漁獲枠に44%の技術的削減を適用して625,000トンに設定し、マアジの1,200,000トンがもたらす安定性を相殺した。

ノルウェーとチリのサケ産業からの購買圧力が重要なボリュームを吸収し、輸出可能な余剰を制限している。同時に、貿易フローは南米での急激な再構成を示している。エクアドルはエビ養殖のための購買ポジションを強化し、ペルー産魚粉の輸入量を17,000トンから46,000トンへと劇的に引き上げた。

最後に、FAOの技術分析は、油脂市場における前例のない屈折を強調している。健康食品や医薬品仕様の魚油は、商業用グレード(feed-grade)を2,044米ドル上回る価格プレミアムを確立しており、高純度セクターにおける需要の硬直性と完全な非弾力性を反映している。

🇨🇳 Chinese Version

秘鲁无限期禁渔与亚洲结构性供应缺口引发全球鱼粉及鱼油价格暴涨

工业化鳀鱼捕捞的暂停加剧了整个水产养殖市场的供应短缺,迫使商业饲料中的添加率降至历史低点,并推高了Omega-3规格副产品的溢价

伦敦(Fish Info & Services) – 全球海洋原料市场在2026年6月期间正面临极度严峻的供应受限局面。南美洲严格的生物管理措施与历史性扩张的水产养殖需求相结合,锁定了结构性供需失衡,使国际价格维持在历史高位。

受海洋异常影响秘鲁延长禁渔期

秘鲁海洋研究院(IMARPE)与国际海洋原料组织(IFFO)确认,无限期延长中北部战略区域鳀鱼(Engraulis ringens)的工业化禁渔令,该措施原定于2026年6月10日到期。

技术监测证实,与沿岸厄尔尼诺现象相关的热异常持续存在。尽管探捕作业检测到的生物量比2025年9月的测量值高出31%(意味着初步理论配额分配为1,914,049公吨),但当前的生物量仍比2025年3月的水准低35%,比过去30年的历史平均水平低17%。鉴于幼鱼比例极高,位于钦博特和卡亚俄的主要直火干燥(SD)鱼粉加工厂继续维持预防性技术停产,以保护资源补充。

作为直接后果,全球累计鱼粉产量同比萎缩26%,全球鱼油供应量则下降14%。这一普遍短缺使国际基准价格保持在每吨2,044美元以上。与此同时,为了在欧盟森林破坏法规(EUDR)的严格要求下确保进入欧洲市场,秘鲁渔业公司Austral Group本月成为该国首家根据Global Feed LCA Institute(GFLI)国际方法验证其海洋原料生命周期评估(LCA)的企业。

水产养殖历史性里程碑与亚洲供应缺口

这一供应紧缩正逢联合国粮农组织(FAO)在其2026年6月17日发布的SOFIA 2026报告中正式指出的行业历史性里程碑:全球水产养殖产量首次突破100,000,000公吨(不含藻类)。这种指数级增长加剧了对海洋投入品的依赖,目前水产养殖吸纳了全球90%以上的鱼粉产量和64%的鱼油产量。

这一压力的影响在IFFO China Summit上得到了严密分析,报告透露亚洲面临严重的水产养殖饲料配方区域供应缺口(Supply Gap),鱼粉年缺口达1,200,000公吨,鱼油年缺口达80,000公吨。

在中国大陆国内市场,需求已碎裂为高度专业化的细分市场(如鳗鱼、虾和加州鲈等品种),这些品种对特定的可消化氨基酸特征有极高要求。饲料制造企业在平衡配方成本上面临严重困难。在青岛和上海港口,进口秘鲁鱼粉(超级品质)的现货价格坚挺在每公吨**22,900至23,000元人民币(约合3,158至3,172美元)**的区间内。

配方的技术困境与替代原料

面对价格危机,Aquafeed.com等技术平台证实,Cargill和Skretting等营养巨头正在执行战略转型,通过使用加工过的陆生动物蛋白,将常规生长饲料中的标准添加率降至历史低点(鲑鳟鱼为14%,虾为12%)。优质鱼粉和高EPA/DHA鱼油库存被严格保留,用于关键生命周期阶段(育苗和前期饲料)的战略性使用。

然而,完全替代带来了严重的陆地环境并发症。斯特林大学于2026年6月在Responsible Seafood Advocate上发表的一项长期研究表明,尽管欧洲行业通过使用大豆蛋白浓缩物和菜籽油进行替代,将每公斤产量的野生鱼使用量减少了59%,但却触发了陆地综合环境足迹的剧烈增长:温室气体(GHG)排放量增加了314%,土地利用增加了594%,水消耗量增加了236%。鉴于昆虫蛋白和微藻尚未达到缓解这些成本的商业规模,该行业决定性地依赖于捕捞副产品(下脚料和内脏)的回收利用,目前这已占全球鱼粉的34%和全球鱼油的54%。

宏观经济调整与副产品扭曲

FAO的GLOBEFISH最新全球平衡报告确认,秘鲁停滞带来的短缺加剧了其他生产国的限制。智利对其鳀鱼配额实施了44%的技术性削减,将其设定为625,000公吨,抵消了1,200,000公吨竹䇲鱼带来的稳定性。

来自挪威和智利鲑鱼产业的购买压力吞噬了关键份额,限制了可出口的剩余量。同时,贸易流向在南美洲呈现剧烈重构:厄瓜多尔巩固了其在虾类养殖中的买方地位,将其对秘鲁鱼粉的进口量从17,000公吨急剧提升至46,000公吨。

最后,FAO的技术分析强调了油脂市场前所未有的折射:具有保健品和药品规格的鱼油已确立了高于商业级(feed-grade)每公吨2,044美元的价格溢价,反映出高纯度领域需求的刚性和完全无弹性。

[email protected]

www.seafood.media

|

.png)

Print

Print