|

Photo: AI/Stockfile/FIS

The production of fishmeal and fish oil faces a high-tension scenario due to restrictions in Peru and historically high prices in China

WORLDWIDE WORLDWIDE

Friday, June 26, 2026, 00:10 (GMT + 9)

Targeted biological bans to protect juvenile anchovy limit spot supply, while Chinese ports consolidate peak quotations of up to $3,461/t under strict commercial discipline.

Click on the image to enlarge it

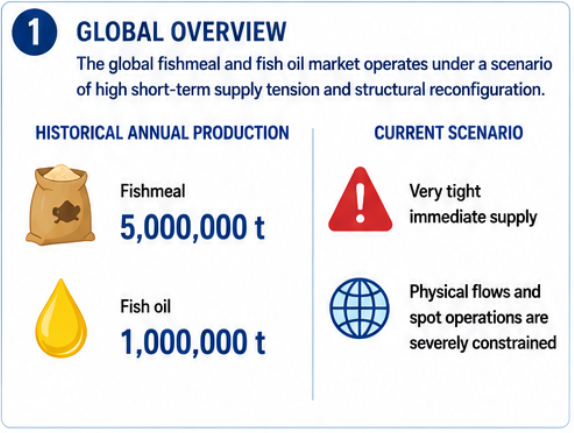

The global fishmeal and fish oil market operates under a scenario of high tension in immediate supply and structural reconfiguration at the close of June 2026. Industry commercial intelligence reports confirm that, despite a macroeconomic stability that places historical annual production at 5,000,000 tonnes of fishmeal and 1,000,000 tonnes of fish oil, immediate physical flows and spot operations are heavily constrained by biological factors at origin and marked commercial prudence in main Asian destinations.

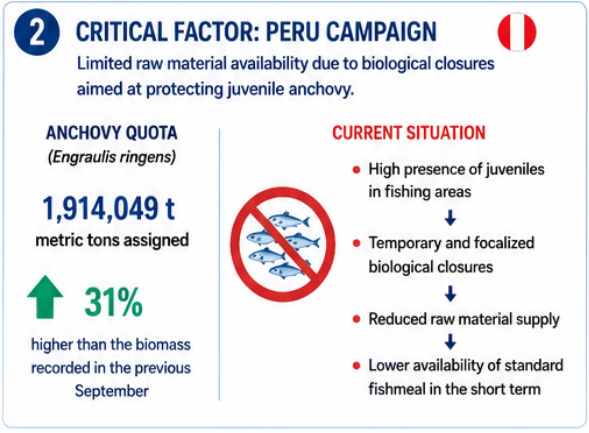

The catching campaign in the north-central region of Peru, the world's largest producer of these inputs, continues to be the critical factor in international trade. Although authorities allocated a quota of 1,914,049 metric tonnes for the species Engraulis ringens (anchovy) —supported by a detected biomass that is 31% higher than that recorded last September—, the operational capacity of reduction plants faces severe bottlenecks. The high presence of juvenile specimens in the fishing areas has forced the implementation of temporary and targeted biological bans, limiting raw material supply and drastically reducing short-term standard meal availability.

Pressure on marine lipids and value added

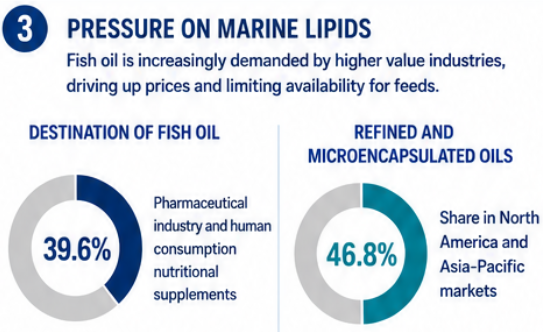

Value chain analysis reveals increasingly intense competition for crude fish oil. The pharmaceutical industry and the human direct consumption supplement sector currently control 39.6% of the global volume of this resource. Within this segment, the development of refined and microencapsulated oils destined for functional foods and advanced human nutrition —highly valued for their oxidative stability— has reached a dominant share of 46.8% in the North American and Asia-Pacific markets.

This strong demand in the human channel, backed by price premiums substantially higher than those of the balanced feed industry, restricts the volume available for pellet coating (aquafeed coating) in low-margin aquaculture. Faced with this shortage in the southern hemisphere, cumulative production in Northern Europe, led by Denmark and Norway, provides stability to the supply of essential fatty acids for the Atlantic salmon (Salmo salar) industry, partially cushioning global price volatility.

China consolidates peak prices and commercial discipline

In this context of restricted supply, the China market has entered a phase of firm consolidation without registering new daily increases, but maintaining historically high levels following the "almost frenetic" behavior of quotations during the previous weeks of June.

According to data from Feedtrade China (中国饲料行业信息网), fishmeal prices have shown absolute uniformity across the country's four strategic import ports, remaining stable in a range of 23,400 to 23,500 RMB per tonne (equivalent to a range of $3,446 to $3,461 per tonne, calculated at a reference exchange rate of $1 ≈ 6.79 RMB):

Local operators and importers interpret this horizontal parity as a sign of strict commercial discipline. There is no evidence of discounts or rebates aimed at accelerating inventory turnover, which confirms the perception of a very tight physical stock and the expectation that market firmness will continue in the short term.

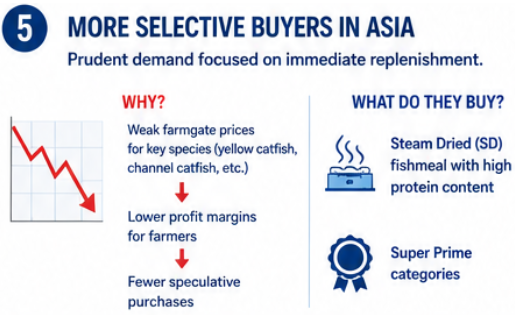

More selective buyers in the Asian market

While physical supply remains limited, demand in China and Vietnam adopts a highly prudent posture. The persistence of weak farm-gate prices for several key commercial species in the Asian market (such as yellow catfish and largemouth bass) has reduced the profit margins of local aquaculturists, curbing speculative purchases.

For this reason, current transactions are carried out in a strictly selective manner focused on immediate replenishment. Buyers concentrate their demand on higher value-added batches, prioritizing steam-dried (SD) meals with high protein concentration and Super Prime categories. These specifications are critical to maximize feed conversion rates and mitigate thermal stress of cultivated species during the current summer season.

International market outlook

The direction of the global market during the close of the month will remain subject to the evolution of the extractive campaign on the Peruvian coast. As long as restrictions aimed at protecting the juvenile biomass of anchovy remain active, exportable availability to Asian and European ports will remain tight.

The stabilization of prices in China ports around $3,446 – $3,461/t confirms that the buying sector validates these record levels as the true reflection of an undersupplied market, remaining expectant of new biological indicators and operational quotas in Peru before modifying their sourcing strategies for the next quarter.

🇯🇵 Japanese Version

ペルーの規制と中国の歴史的高値により、魚粉・魚油生産は高緊張シナリオに直面

未成魚のカタクチイワシを保護するための局所的な禁漁規制によりスポット供給が制限される一方、中国の港湾では厳格な商業規律のもと、最高3,461米ドル/tに達する価格提示が定着。

魚粉および魚油のグローバル市場は、2026年6月末時点で、当面の供給における高い緊張と構造的な再編成のシナリオのもとで推移しています。業界の商業情報レポートによると、歴史的な年間生産量が魚粉5,000,000トン、魚油1,000,000トンというマクロ経済的な安定性にあるにもかかわらず、供給地における生物学的要因と主要なアジアの目的地における顕著な商業的慎重さにより、当面の物理的な流通とスポット取引は強力に制約されています。

これら原料の世界最大の生産国であるペルーの中北部地域における漁獲キャンペーンは、引き続き国際貿易の極めて重要な要因となっています。当局はEngraulis ringens(カタクチイワシ)に対して1,914,049メートルトンの枠を割り当て、これは昨年9月に記録されたものより31%高い推定バイオマスに裏付けられているものの、魚粉加工工場の操業度は深刻なボトルネックに直面しています。漁場における未成魚の割合が非常に高いため、一時的かつ局所的な禁漁措置の実施を余儀なくされており、原料の供給が制限され、短期的にはスタンダード魚粉の供給可能性が劇的に減少しています。

海洋脂質への圧力と付加価値

バリューチェーンの分析によると、粗製魚油を巡る競争はますます激化しています。製薬業界および人間の直接摂取用サプリメントセクターは、現在、この資源の世界的な量の39.6%をコントロールしています。このセグメント内において、機能性食品や高度な人間栄養向けに指定された、酸化安定性で高く評価されている精製・マイクロカプセル化オイルは、北米およびアジア太平洋市場において46.8%の支配的なシェアに達しています。

この人間向けチャネルにおける強力な需要は、配合飼料業界のものよりも大幅に高い価格プレミアムに支えられており、低利益の養殖業におけるペレットのコーティング(aquafeed coating)に使用可能な量を制限しています。南半球におけるこの不足に直面し、デンマークやノルウェーが牽引する北欧の累積生産は、大西洋サケ(Salmo salar)業界向けの必須脂肪酸の供給に安定性をもたらし、世界的な価格変動を部分的に緩和しています。

中国は最高価格と商業規律を維持

供給が制限されるこの文脈において、中国市場は、日々の新たな上昇を記録することなく強固な維持局面に入っているものの、これまでの6月の数週間に見られた価格提示の「狂気じみた」動向を経て、歴史的に高い水準を維持しています。

Feedtrade China(中国饲料行业信息网)のデータによると、魚粉価格は同国の4つの戦略的な輸入港湾すべてにおいて絶対的な一律性を示しており、1トンあたり23,400〜23,500人民元(参照為替レート1米ドル≒6.79人民元で計算すると、1トンあたり3,446〜3,461米ドルの範囲に相当)の範囲で安定しています。)

現地の業者や輸入業者は、この水平的なパリティ(同等性)を厳格な商業規律の兆候と解釈しています。在庫回転を加速させることを目的とした割引や値下げの証拠はなく、これは物理的な在庫が非常に逼迫しているという認識と、市場の堅調さが短期的に継続するという予想を裏付けています。

アジア市場におけるより選択的な買い手

物理的な供給が限られたままである一方、中国およびベトナムにおける需要は極めて慎重な姿勢を採用しています。アジア市場におけるいくつかの主要な商業種(イエローキャットフィッシュやオオクチバスなど)の池揚価格が依然として弱い状態が続いているため、現地の養殖業者の利益マージンが減少しており、投機的な購入が抑制されています。

このため、現在の取引は、当面の補充に焦点を当てた厳格に選択的な方法で行われています。買い手は需要をより高付加価値なロットに集中させており、高タンパク質濃度でスーパープライムカテゴリーの蒸気乾燥(SD)魚粉を優先しています。これらの仕様は、現在の夏季シーズン中における飼料効率を最大化し、養殖種の熱ストレスを緩和するために極めて重要です。

国際市場の見通し

今月末のグローバル市場の方向性は、引き続きペルー沿岸における漁獲キャンペーンの動向に左右されることになります。カタクチイワシの未成魚バイオマスを保護することを目的とした規制が有効である限り、アジアおよびヨーロッパの港湾への輸出可能性は限られた状態が続くでしょう。

中国の港湾における価格が3,446〜3,461米ドル/t前後で安定していることは、購買セクターがこれらの記録的な水準を供給不足の市場の忠実な反映として容認していることを裏付けており、次の四半期に向けた調達戦略を再定義する前に、ペルーにおける新たな生物学的指標や操業枠を待つ姿勢を維持しています。

🇨🇳 Chinese Version

受秘鲁禁渔限制及中国历史高价影响,鱼粉与鱼油生产面临高度紧张局势

旨在保护幼鳀鱼的局部靶向禁渔限制了现货供应,而中国港口在严格的商业纪律下,将最高报价稳定在 3,461 美元/吨。

截至 2026 年 6 月底,全球鱼粉和鱼油市场在当期供应高度紧张和结构性重组的局势下运行。行业商业情报报告证实,尽管宏观经济总体稳定,历史年产量保持在鱼粉 5,000,000 吨和鱼油 1,000,000 吨,但由于产地的生物学因素以及主要亚洲目的地的显著商业谨慎态度,当期的实物流量和现货交易受到严重制约。

作为这些原料的世界最大生产国,秘鲁中北部地区的捕捞活动仍是影响国际贸易的关键因素。尽管当局针对Engraulis ringens(鳀鱼)分配了 1,914,049 公吨的配额——该配额得到了比去年 9 月记录高出 31% 的推测生物量的支持——但鱼粉加工厂的运营仍面临严重的瓶颈。捕捞区内高比例的幼鱼导致管理部门不得不实施临时和局部性的生物禁渔,限制了原材料供应,并急剧减少了短期内标准鱼粉的可供应量。

Marine Lipids 压力与增值

价值链分析显示,围绕粗鱼油的竞争日益激烈。医药行业和人类直接食用营养补充剂领域目前控制着该资源全球总量的 39.6%。在此细分市场中,由于在功能性食品和高级人类营养中因抗氧化稳定性而受到高度评价,专门用于这些领域的精炼和微胶囊化鱼油在北美和亚太市场已达到 46.8% 的主导份额。

人类消费渠道的强劲需求得到了远高于配合饲料行业的溢价支持,从而限制了低利润养殖业中用于颗粒涂层(aquafeed coating)的可用鱼油量。面对南半球的这一短缺,以丹麦和挪威为首的北欧累计产量为大西洋鲑(Salmo salar)产业提供了必需脂肪酸的供应稳定性,部分缓冲了全球价格 seasonal 波动。

中国稳定最高价格与商业纪律

在供应受限的背景下,中国市场已进入坚固的盘整阶段,未记录新的每日上涨,但在经历前几周6月报价“近乎疯狂”的走势后,依然保持在历史高位。

根据中国饲料行业信息网(Feedtrade China)的数据,鱼粉价格在该国四个战略性进口港口表现出绝对的一致性,稳定在每吨 23,400 至 23,500 人民币的区间(按 1 美元 ≈ 6.79 人民币的参考汇率计算,约合每吨 3,446 至 3,461 美元):

当地贸易商和进口商将这种横向持平视为严格商业纪律的信号。没有证据表明存在旨在加速库存周转的让利或打折行为,这印证了实物库存非常紧张的观点,以及市场坚挺势头将在短期内持续的预期。

亚洲市场买家更具选择性

在实物供应维持受限的同时,中国和越南的需求采取了高度审慎的姿态。亚洲市场几种主要商业品种(如黄颡鱼和大口黑鲈)的出塘价格持续低迷,压缩了当地养殖户的利润空间,从而抑制了投机性采购。

因此,当前的交易表现为专注于即期补库的严格选择性方式。买家将需求集中在更高附加值的批次上,优先选择具有高蛋白质浓度和超级至尊(Super Prime)级别的蒸汽干燥(SD)鱼粉。这些指标对于在当前夏季提高饲料转化率和减轻养殖品种的热应激至关重要。

国际市场展望

月底全球市场的走向将继续取决于秘鲁沿海捕捞活动的进展。只要旨在保护鳀鱼幼鱼生物量的限制措施保持出台状态,对亚洲和欧洲港口的出口可用量将持续受限。

中国港口价格稳定在 3,446 – 3,461 美元/吨 附近,证实了买方市场认可这些创纪录的水准是对供不应求市场的真实反映,在重新定义下一季度的采购战略之前,各方仍对秘鲁新的生物学指标和运营配额保持观望。

|

.png)

Print

Print